MID-SHIP Petcoke Report – July 14, 2025

July 14, 2025

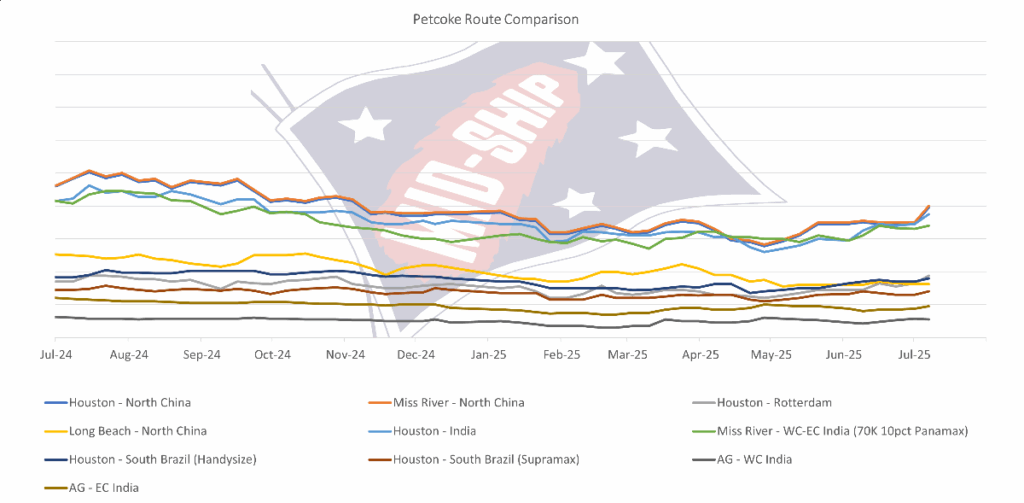

Market overview:

The Capesize market commenced the week on a positive note, despite relatively subdued activity levels. The BCI 5TC recorded a significant increase of $2,180, reaching $19,633, indicating robust sentiment across both the Atlantic and Pacific basins. The Panamax and Supramax segments maintained their upward momentum at the week’s outset, supported by strong demand in the US Gulf and East Coast South America regions. Meanwhile, the Handyside market exhibited signs of revitalization, with more robust trading activity observed in Asia.

The U.S. Administration increased trade tensions again by announcing a 30% tariff on imports from the EU and Mexico, effective August 1st. On July 14, 2025, President Trump threatened to impose 100% secondary tariffs on countries and companies purchasing Russian exports (particularly oil, gas, and uranium) if Russia does not reach a peace agreement with Ukraine within 50 days (by approximately September 2, 2025). These tariffs would affect major Russian oil buyers like China, India, Brazil, and Turkey, as well as some EU countries such as Hungary, Slovakia, and the Czech Republic.

The new U.S. legislation (OBBB) phases out tax credits for wind and solar, which may diminish their economic edge over coal. It also adds metallurgical coal that’s used to make steel to the list critical minerals qualifying for tax credits.

Our market, while relatively firm for mid-July and the summer season, is once again in a wait-and-see mode, with expectations of potential shifts due to geopolitical and economic factors, resulting from renewed tariff complexity this week.

Subscribe below to receive the full report.