MID-SHIP Petcoke Report – February 5, 2026

February 5, 2026

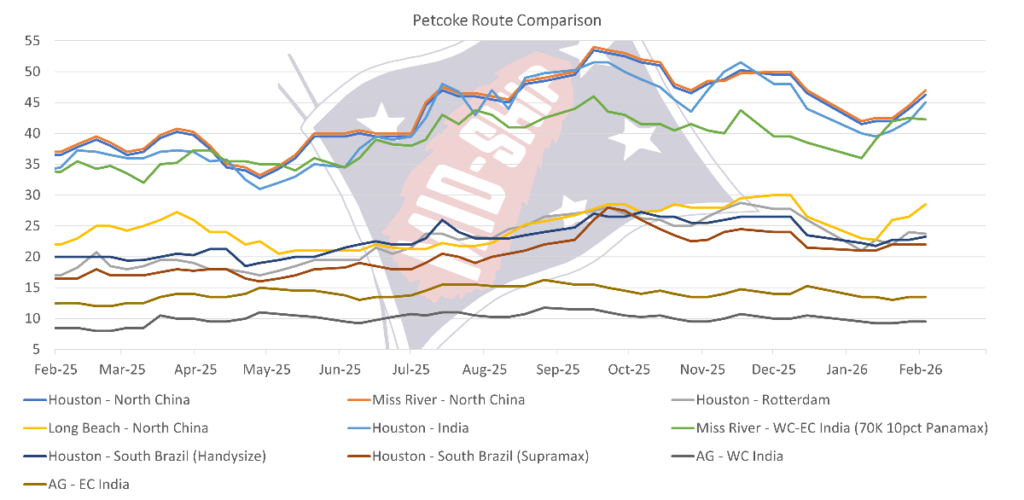

Market overview:

The dry bulk market experienced a subdued session overall to start this week, with activity levels remaining thin across most segments. Sentiment varied by basin, though the Atlantic continued to display comparatively firmer undertones than Asia.

In the Handysize sector, conditions remained quiet, with limited fresh fixing emerging. The BHSI closed at 626, while the 7TC edged higher by $74 to $11,259. In the Continent and Mediterranean, activity was minimal, and the market appeared broadly balanced, with rates marginally firmer than recent levels. By contrast, the U.S. Gulf and South Atlantic continued to show gradual upward momentum, fostering cautious optimism among market participants despite the lack of concrete fixtures. A 37,000 DWT vessel was reportedly fixed by Cargill for a Santos–Croatia voyage at $20,500, although further details were not disclosed. In Asia, trading was muted, with a relatively shorter tonnage list offset by little change in the cargo book.

The Supramax/Ultramax segment saw another information-light day. The Atlantic basin remained relatively buoyant, supported by improving sentiment in several areas, though some participants suggested the U.S. Gulf may be approaching a near-term bottom as fresh fixing data remained scarce. The South Atlantic stayed largely positional, yet modest upward momentum persisted. A 64,000 DWT vessel was heard placed on subjects for an EC South America–Singapore/Japan trip at mid $16,000s plus mid $600,000s ballast bonus, though no confirmation followed. In Asia, brokers described a slower session, with recent gains in the northern regions easing. Period activity provided some support, with talk of a 63,000 DWT open Zhoushan fixing 13 – 15 months in the upper $15,000s. The 11TC average finished the day up $136 at $13,691.

Conditions softened further in the Panamax sector, where the BPI time charter average slipped $220 to $15,515, reflecting a weaker trading day overall. Atlantic sentiment came under pressure as several core charterers remained absent, while limited transatlantic and fronthaul stems circulated. Many charterers appeared well covered through backstops, and tonnage lists lengthened as additional prompt vessels entered the market. Fronthaul demand remained subdued, with mineral fronthaul cargoes being offered at last-done levels but failing to attract interest. In Asia, the market also trended softer, with marginally lower levels and a thinner cargo book, particularly from NoPac and East Coast Australia. That said, modern and larger tonnage continued to attract interest and may still command a premium over base levels.

Subscribe below to receive the full report.