MID-SHIP Cement Report – February 26, 2026

February 26, 2026

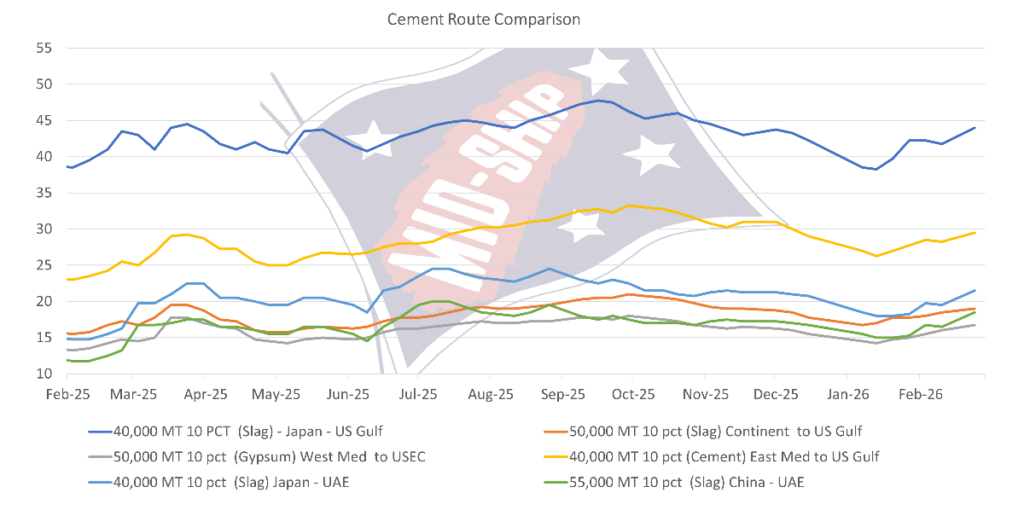

Market Overview:

Dry bulk freight markets delivered a mixed but generally steady performance today, with trends varying across vessel classes and regions. In the Capesize segment, the BCI 5TC eased marginally by $23 to $29,088, reflecting a Pacific market that has largely stabilized. Activity remained consistent, with major miners and operators concluding fixtures in the low to mid $10s range, keeping the C5 index broadly flat at $10.174. The Atlantic was more subdued, particularly ex Brazil and West Africa, where a wide bid offer gap limited concluded business despite a slight uptick in the C3 index. Growing tonnage in the North Atlantic also contributed to softer sentiment. Period interest remained steady, highlighted by Classic’s 11 – 13 month fixture of the NGM Bond at $31,500.

Panamax market dynamics diverged sharply between basins, with Atlantic softness offset by continued strength in the Pacific. In the Atlantic, accumulating prompt tonnage and insufficient fresh enquiry placed downward pressure on transatlantic routes, resulting in a $186 decline in the P1A index. By contrast, the Pacific maintained a firm tone supported by tight vessel supply and healthy demand across Indonesia, Australia, and the North Pacific; this lifted the P3A index by $329. The firmer Pacific environment also supported the backhaul market, where the P4 rose by $300. Period sentiment remained constructive, with the Sakizaya Diamond fixing 11 – 13 months at $17,500, helping the P5TC average rise to $16,793.

The Supramax and Handysize sectors exhibited a more balanced and constructive tone across both basins. Supramaxes saw the 11TC average increase by $485 to $15,382, with stable Atlantic fundamentals complemented by stronger activity in Asia — particularly from the North Pacific and South Indonesia coal trades. Period interest remained present, with the Belforce securing a 4 – 6-month charter at $16,750. The Handysize market also strengthened, with the BHSI adding 13 points to 724 as sentiment improved in both the Continent–Mediterranean and Asian regions. Firmer Pacific demand and tighter tonnage supported a range of spot and short period fixtures, including the Guzide to the Arabian Gulf and multiple forward coverage enquiries across the basin.

Subscribe below to receive the full report.