MID-SHIP Petcoke Report – March 19, 2026

March 19, 2026

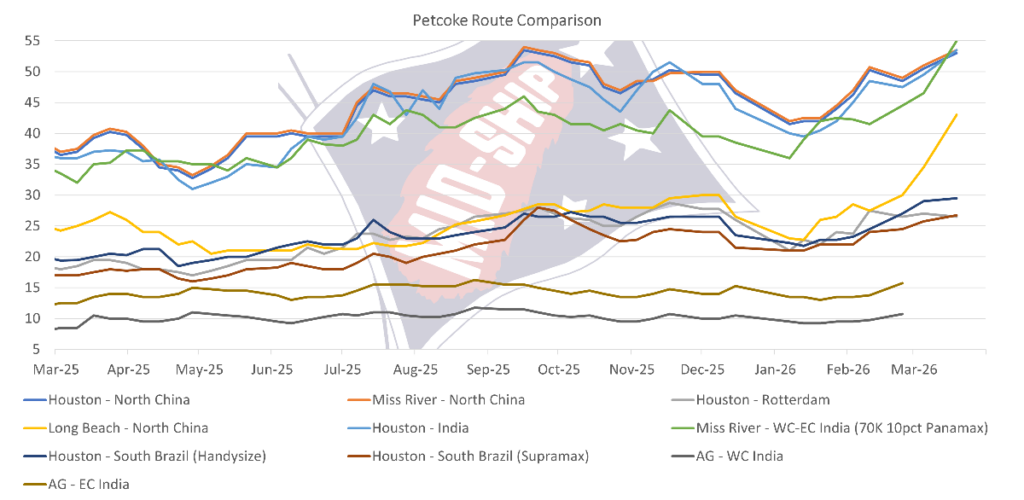

Market overview:

Handysize: ▼

Handysize markets continued to drift, with subdued activity and softening sentiment evident across both basins. The Continent and Mediterranean held largely steady, while the South Atlantic and U.S. Gulf remained pressured by thin cargo availability. In the Pacific, owners showed pockets of resistance, but uncertain demand capped any upside, keeping rates broadly rangebound. Fixture flow was limited, with most reported business concluded on subjects and offering little signal of near-term improvement.

Supramax: ▼

Supramax conditions remained under pressure, with limited fresh enquiry and a lack of volume continuing to weigh on rates across most regions. The U.S. Gulf and South Atlantic saw little new business, pushing rates below recent benchmarks, while the Continent–Mediterranean remained flat amid muted interest. In Asia, sentiment stayed weak as tightening cargo volumes, increasing vessel availability, and high bunker costs curtailed upside. One longer-haul fixture from South Africa to China provided a brief highlight, but overall market direction remains defensive.

Panamax: ▲

The Panamax market showed clear signs of strengthening, led by improved demand in the Atlantic for both fronthaul and transatlantic business, allowing owners to defend firmer rate ideas despite an otherwise balanced tonnage list. Index gains across the Atlantic routes underlined the improved tone, while Asia followed suit, supported by stronger cargo flows from Indonesia into India. Fixture activity was steady across both basins, with multiple vessels reported fixed or on subjects for fronthaul, round-trip, and grains employment, reinforcing the view of gradually improving momentum.

Capesize: ▼

Capesize sentiment cooled as the market consolidated, with transpacific weakness offsetting firmer transatlantic and fronthaul activity.

Subscribe below to receive the full report.