MID-SHIP Cement Report – Nov 26, 2024

November 26, 2024

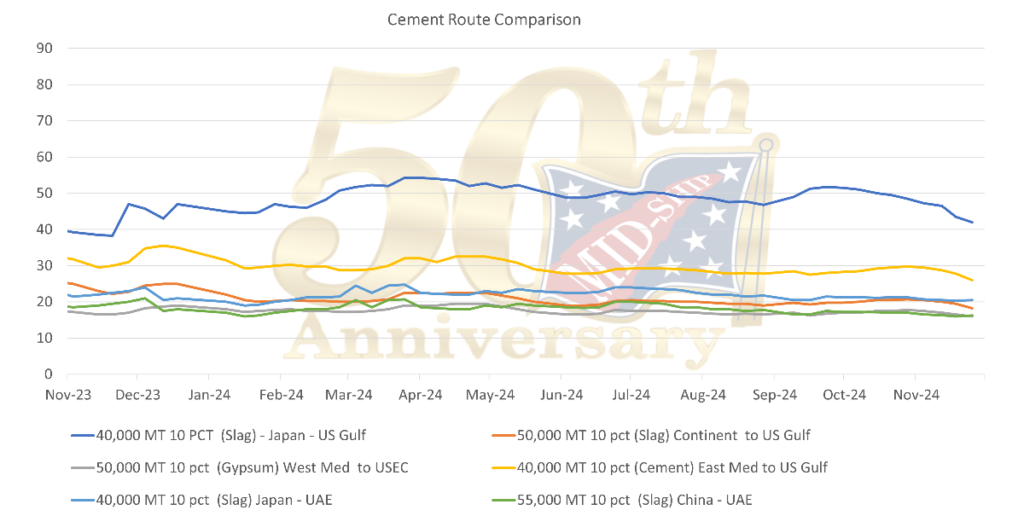

Market Overview:

Last week, the Cape size market experienced a significant decline in rates, aligning with the broader trend in the dry bulk market, largely due to weak demand in the Panamax segment. The Panamax, Supramax, and Handysize segments continued to trade within a narrow range, with an oversupply of vessels exerting pressure across all segments.

Despite concerns about demand, iron ore production remains strong. Major producers such as BHP, Fortescue, and Rio Tinto have either maintained or increased their production levels. Iron ore prices are expected to be volatile due to slowing growth in steel production and increased output from global producers. According to the International Energy Agency (IEA), global coal demand reached an all-time high this year. Steam coal is expected to decline by low single-digit percentages annually while coking coal looks to be flat through 2026.

The robust market conditions have discouraged the scrapping of older vessels, resulting in an aging fleet. However, high secondhand prices, until recently, have encouraged some owners to invest in new builds. Recently, we have observed a decline in secondhand prices.

Approximately 30% of the Handy fleet, 25% of the Supra/Ultra fleet, and just over 25% of the Panamax fleet are 15 years old or older. About half of these percentage numbers represent ships 20 years or older.

Subscribe below to receive the full report.