December 6, 2024

The Baltic Exchange Main Overall Index hit new lows this week, levels not seen since September 2023.

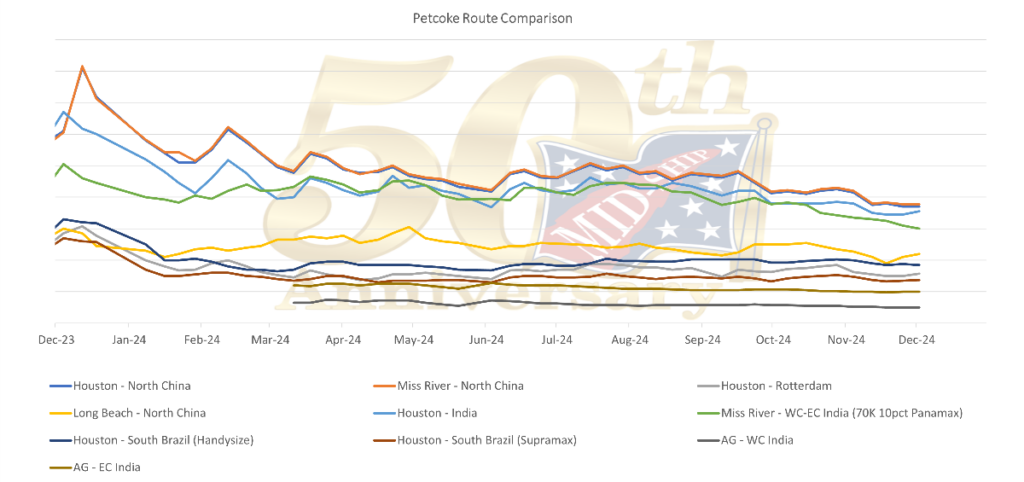

Cape Market continues to struggle with rates the bell weather Brazilian Iron ore flows, all trading at a significant discount this week. Brazil/Europe Cape freight flows are trading now under $10 per metric ton, and front haul movements to China will soon be trading under $18 per metric ton (remember, as of 1-2 months ago, this trade was almost 10 USD more a ton then today’s spot which shows the headwinds the South Atlantic Cape Market has had in the 4th quarter this year).

There are no signs of a recovery in the Panamax market anytime soon. The Time Charter Average is currently trading at half its value compared to December last year, approaching the next support level of $8,000 per day. In the Pacific Basin, despite Beijing’s efforts to sustain the market, freight rates have now leveled off with those in the Atlantic Basin. The market is so depressed that ship owners are willing to compete with the Capesize market to secure employment for their vessels, leading to several Capesize cargoes being split into Panamaxes.

Transatlantic voyages Supramax vessels have been ticking up to around USD 19,000 per day, while front hauls are around USD 20,000 per day. However, many feel that rates may flatten out as the calendar turns to December. The South Atlantic has been facing downward pressure due to a lack of fresh cargoes from East Coast South America. The Continent has not had much activity, while the Mediterranean and the Black Sea have been depressed, with backhaul rates lower than the handy backhaul rates. The market in the Pacific has seen less activity for backhaul cargoes, but there has been more demand for Nopac round voyages.

The past two weeks in the Atlantic market have been active but varied depending on the region. In the US Gulf, the Handysize market remained steady despite a brief increase in activity after the Thanksgiving holiday. In the South Atlantic, the pre-holiday rush created a strong wave of activity, with healthy demand for premium trades to destinations like the West Coast of South America; however, logistical challenges, including weather disruptions in ECSA, led to some delays and renegotiations. In the Far East, steel cargoes are surfacing again in several different directions. However, with a lagging Supramax market, the bigger ships are starting to compete with larger Handies on these backhauls. SE Asia has gained some momentum with coal and wood pellet orders and is looking to source prompt ships.

The South Atlantic shipping markets experienced a volatile week across the Cape, Panamax and Ultra-Supra sizes, with downward trends dominating due to a mix of external factors and bearish market dynamics.

With the UAE celebrating National Day 2024 on Monday and Tuesday, it is no surprise that the Indian Ocean market experienced a notably sluggish start to the week. Festivities and public holidays across the region temporarily reduced commercial activity, leading to a slower pace in the market, which is reflected in the limited availability of cargo entering the market.

When speaking with vessel owners in the Handy, Supra, and Ultra segments in Australia and the surrounding region, we sense a positive atmosphere and some optimism regarding a potential market uptick for the year’s end. However, when looking at the spot Baltic indexes, futures, and oil prices, it appears that the positive sentiment may be more linked to the upcoming holiday season rather than solid market fundamentals.

Regionally, Handy, Supra, and Ultra rates have dropped significantly over the past couple of weeks (see below), and futures prices have also fallen sharply in both segments. Decline in oil prices is also adding downward pressure to freight levels and we are not seeing a noticeable uptick in market orders, making it challenging to share in the optimism.

In the inland barge markets, the USDA reported that grain barge freight from St. Louis to NOLA was trading at 399% of tariff as of November 26, 2024, a 6% increase from the same week last year. Grain barge movements on the Mississippi River for the week ending November 23 were 17% higher than the three-year average for the same week.

Subscribe below to receive the full report.