MID-SHIP Report: Dry Bulk Freight Market – May 7, 2025

May 7, 2025

The Cape market continues to soften across both basins, with Chinese dry bulk demand under pressure and seaborne iron ore volumes plateauing in 2025. The outcome of U.S.-China trade negotiations remains critical to China, the broader dry bulk market, and the Cape market specifically. Despite a positive run since April 23, momentum was dampened by last week’s May Day holidays.

The Panamax Time Charter Average has remained stable at approximately $12,000 daily for the past two weeks. However, shipowners are offering discounts on forward positions, signaling caution and potential further softening before recovery. In the Atlantic basin, previously trading at a discount to the Pacific, a vessel shortage has reversed this trend, with the Atlantic now commanding a 20% premium, though liquidity remains lower. South America is positioning to capitalize on U.S. tariffs and the upcoming grain season, despite subdued Chinese iron ore imports due to economic challenges. Strong soy imports into China, driven by Brazil’s large harvest, are expected to continue into Q2, supporting Panamax tonne-mile demand and freight rates.

After several weeks in decline, the Supramax market seems to have stabilized in certain pockets and strengthened in others as many feel that this market segment hit bottom and is starting into a period of limited recovery. Trans Atlantic rates have risen buoyed by increased demand in East Coast South America – heavily supported by grain exports. While there has been a noticeable drop in pricing for trips inbound to the Atlantic and from the Mediterranean, this is probably attributable to a combination of reduced demand and a resumption of more traditional backhaul trading with USG pricing showing signs of recovery.

Handy pricing and expectations are cloudier than what we are currently seeing for the Supramax sector. While there are similar patterns of small recoveries in the Atlantic, repositioning pricing is still relatively low and has not rebounded in the same way. Persistent holidays over the last 2 weeks have added to a lackluster recovery and general demand factors for smaller bulk are crimping demand for these ships. This is one area where tariff discussions may be having a larger impact than originally predicted.

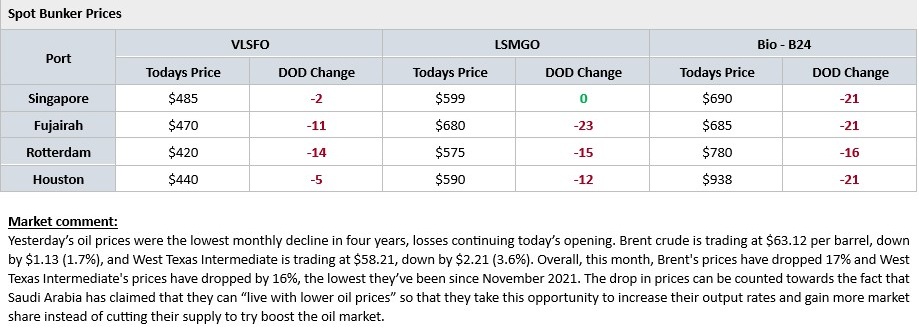

OPEC+ announced an output increase, adding downward pressure on oil prices amid macroeconomic concerns.

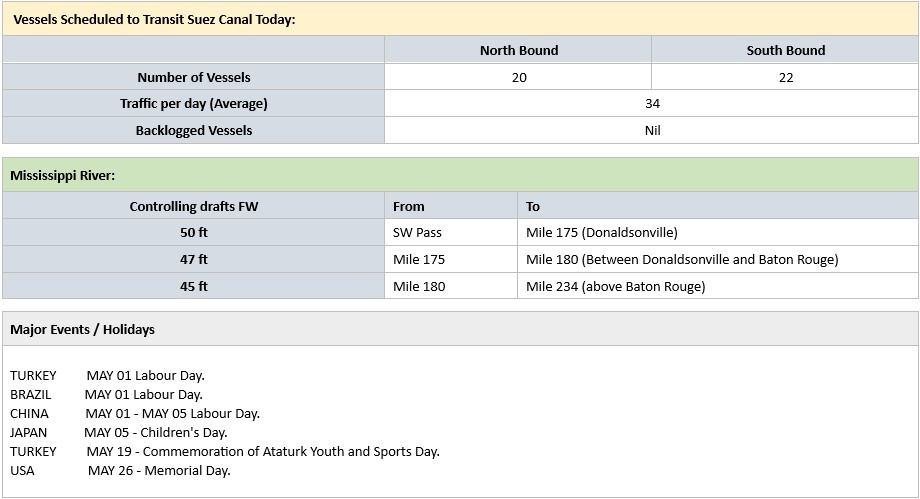

In the U.S. domestic market, high water restrictions persist along the Mississippi River, with levels not expected to fall below the high-water threshold until late May. Heavy delays are anticipated for northbound Gulf departures through May, compounded by severe delays from Cairo to Chicago following the Lockport Lock closure. Carriers are addressing backlogs, but tow size and daylight restrictions continue to slow progress. The USDA reported grain barge freight for St. Louis to New Orleans at 350.94% of tariff for the week ending April 29, 2025. Barged grain movements totaled 670,133 tons for the week ending April 26, up 43% from the prior week and 52% from the same period last year.

Subscribe below to receive the full report.